27-02-25

Asset reconciliation is a crucial accounting process that ensures a company’s financial records accurately reflect its physical and financial assets. This process involves comparing internal asset records with external data, such as bank statements, invoices, and physical inventory counts, to identify discrepancies and maintain financial accuracy.

The primary goal of asset reconciliation is to detect and resolve inconsistencies between recorded and actual assets. This ensures accurate financial reporting, compliance with accounting standards, and a clear understanding of an organization’s financial position.

While asset reconciliation is essential, bookkeepers and accountants often make mistakes that can lead to inaccurate financial statements, cash flow issues, and regulatory non-compliance. Below are some of the most common errors:

Bookkeepers may incorrectly classify assets, such as recording short-term assets as long-term or failing to distinguish between tangible and intangible assets. This misclassification can distort financial reporting and impact decision-making.

Depreciation adjustments are critical in maintaining accurate asset values. Accountants who neglect to update depreciation records may overstate asset values, leading to inflated financial statements.

When a company sells, retires, or disposes of assets, these changes must be accurately recorded. Failing to remove disposed assets from the books can lead to inflated asset values and inaccurate balance sheets.

Duplicate entries can occur when bookkeepers manually record asset transactions without cross-checking previous entries. This results in inflated asset values and incorrect financial statements.

Irregular asset reconciliation increases the likelihood of errors and financial misstatements. Many businesses only perform reconciliation during audits or tax season, which can lead to untracked discrepancies and increased risks.

Errors in asset valuation, such as incorrect fair market value assessments or miscalculating purchase prices, can lead to incorrect financial reports and tax misstatements.

To maintain accurate financial records, businesses must implement effective asset reconciliation procedures. Here are the best practices to follow:

Develop a standardized reconciliation process that includes step-by-step guidelines for verifying and adjusting asset records. This should include scheduled reconciliations, assigned responsibilities, and clear documentation procedures.

Investing in accounting software like QuickBooks, Xero, Zoho, or Sage can automate reconciliation and reduce human errors. These platforms offer built-in asset management and depreciation tracking tools.

Perform monthly or quarterly asset reconciliations to detect and resolve discrepancies early. Consistent reconciliation ensures accurate financial statements and smooth audits.

Keep thorough records of all asset purchases, transfers, and disposals. Cross-check invoices, receipts, and sales agreements to ensure accurate documentation.

To prevent fraud and errors, businesses should implement internal controls such as segregation of duties, audit trails, and approval processes for asset-related transactions.

Regularly update depreciation schedules to reflect changes in asset value. This ensures accurate financial reporting and prevents overstated asset values.

Educate your finance team on best reconciliation practices to reduce errors. Proper training in asset classification, depreciation tracking, and record-keeping is essential.

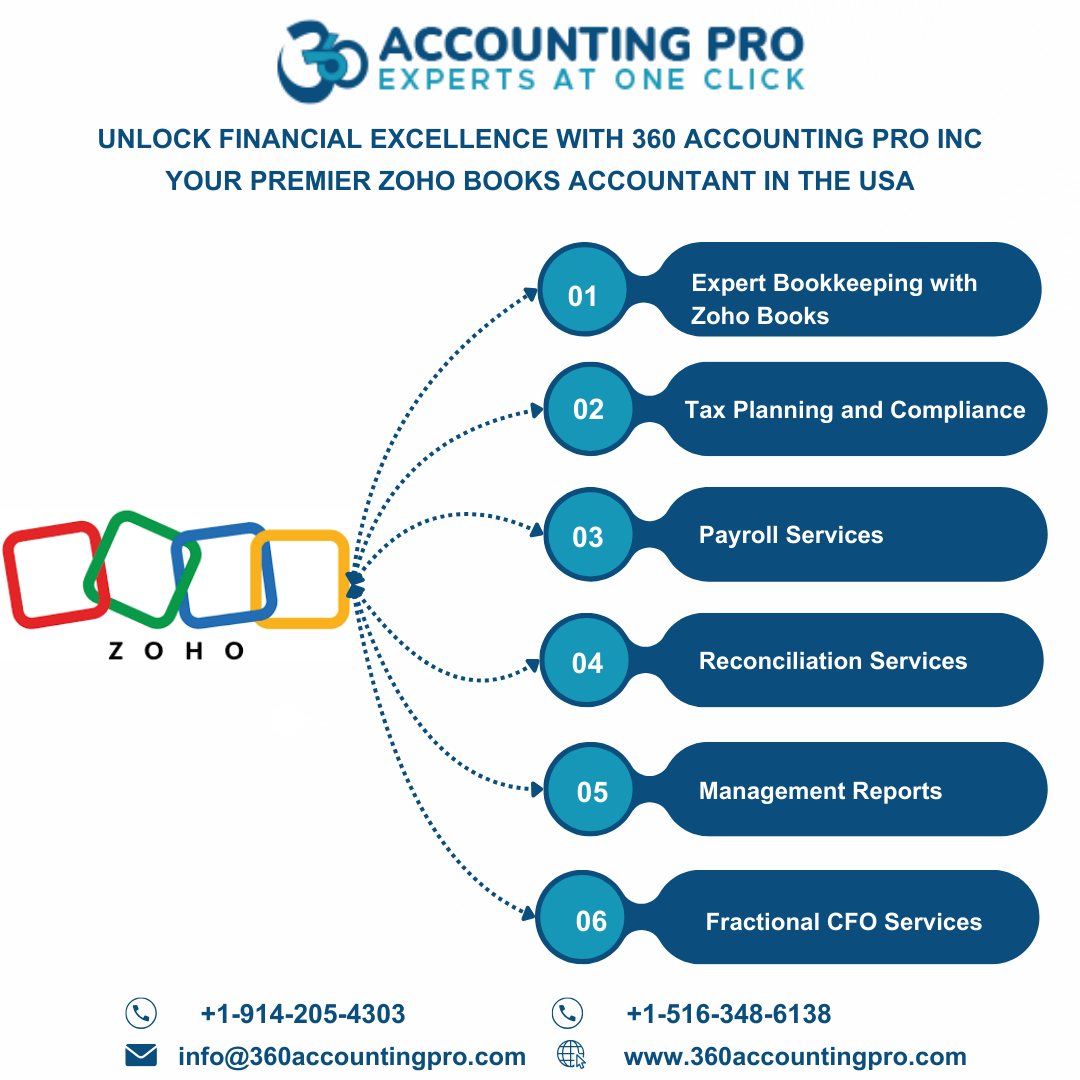

At 360 Accounting Pro Inc., we specialize in accurate asset reconciliation to help businesses maintain financial transparency and compliance. Our expert accountants ensure that your asset records align with financial statements, reducing the risk of discrepancies.

Detailed Asset Tracking: We verify and categorize all business assets for accurate record-keeping.

Depreciation Management: Our team ensures depreciation schedules are up-to-date and compliant with accounting standards.

Automated Reconciliation Solutions: We integrate accounting software to automate reconciliation and reduce manual errors.

Audit Preparation: We provide complete documentation and reconciliation reports to streamline audits.

Error Detection and Correction: Our team reviews past records, identifies errors, and makes necessary adjustments to correct financial statements.

Asset reconciliation is a critical component of financial management that ensures a business’s assets are accurately recorded and reported. Avoiding common reconciliation mistakes and implementing best practices can help maintain financial accuracy and compliance.

If you need professional assistance in asset reconciliation, depreciation tracking, or financial reporting, 360 Accounting Pro Inc. is here to help. Our experts ensure seamless reconciliation, preventing costly errors and maintaining accurate financial records.

Contact us today to optimize your asset reconciliation process and keep your business finances in perfect order. Visit www.360accountingpro.com for more details.

Tags : #AssetReconciliation, #FinancialManagement, #AccountingProcess, #FinancialAccuracy, #AssetTracking, #DepreciationManagement, #ReconciliationMistakes, #AccountingErrors, #FinancialCompliance, #AccountingBestPractices, #BookkeepingTips, #BusinessAccounting, #AuditPreparation

.jpg)

.jpg)

.png)

.png)

.png)

.jpg)

.jpg)

.jpg)

).jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.png)

.jpg)

.jpg)

.jpg)

.jpg)

.png)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.png)

.jpg)

.jpg)

.jpg)

.jpg)

.png)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.png)

.jpg)

5.png)

1.png)

2.png)

3.png)

2.png)

4.png)

2.png)

1.png)

1.png)

3.png)

2.png)

1.png)

2.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

1.png)

1.png)

.png)

.jpg)

.png)

.png)

Get A Quote

Get A Quote

Leave A Comment