17-12-24

What is Bank Reconciliation

Bank reconciliation is the process of comparing a company's internal financial records with bank statements to ensure accuracy. It helps businesses track transactions, detect errors, and prevent fraud. Conducting a step-by-step bank reconciliation regularly ensures that all financial records are up to date and that discrepancies are addressed promptly.

At 360 Accounting Pro Inc. we specialize in simplifying the bank reconciliation process, ensuring businesses maintain accurate records with minimal effort.

Performing bank reconciliations is crucial for maintaining the integrity of financial records. Here are some key benefits

Ensures accuracy by confirming that financial records align with actual bank transactions

Detects fraud by identifying unauthorized transactions and discrepancies

Improves cash flow management by helping businesses plan and manage cash flow efficiently

Aids in compliance by ensuring regulatory and tax compliance with precise financial records

To complete a bank reconciliation successfully follow these key steps

Step One Gather Necessary Documents

Before starting the reconciliation collect the required documents including

Latest bank statement with the most recent bank transactions report

General ledger records from internal accounting books or reports

Outstanding checks and deposits for any pending financial transactions

Step Two Compare Opening Balances

Ensure the opening balance in accounting records matches the beginning balance on the bank statement. If there is a mismatch investigate and correct any errors before proceeding.

Step Three Match Transactions

Compare transactions line by line between the bank statement and internal records

Check deposits to ensure all deposits in the bank match the cash receipts in the books

Review withdrawals to verify all withdrawals checks and electronic transfers are recorded

Match bank fees and interest by recording any bank charges interest income or other adjustments

Step Four Identify Outstanding Items

Identify transactions in the business records that have not yet cleared the bank and vice versa

Outstanding checks issued but not yet cashed

Pending deposits received but not reflected in the bank statement

Bank charges and adjustments for unrecorded fees penalties or interest

Step Five Adjust and Reconcile Balances

After making necessary adjustments the adjusted book balance should match the bank statement’s ending balance. If differences persist

Double-check entries for missing transactions or errors

Review transaction dates for potential posting delays

Investigate unauthorized or suspicious transactions

Not reconciling regularly as monthly reconciliations help detect errors early

Ignoring small differences as minor discrepancies can accumulate over time

Inconsistent record-keeping as incomplete transaction records complicate reconciliations

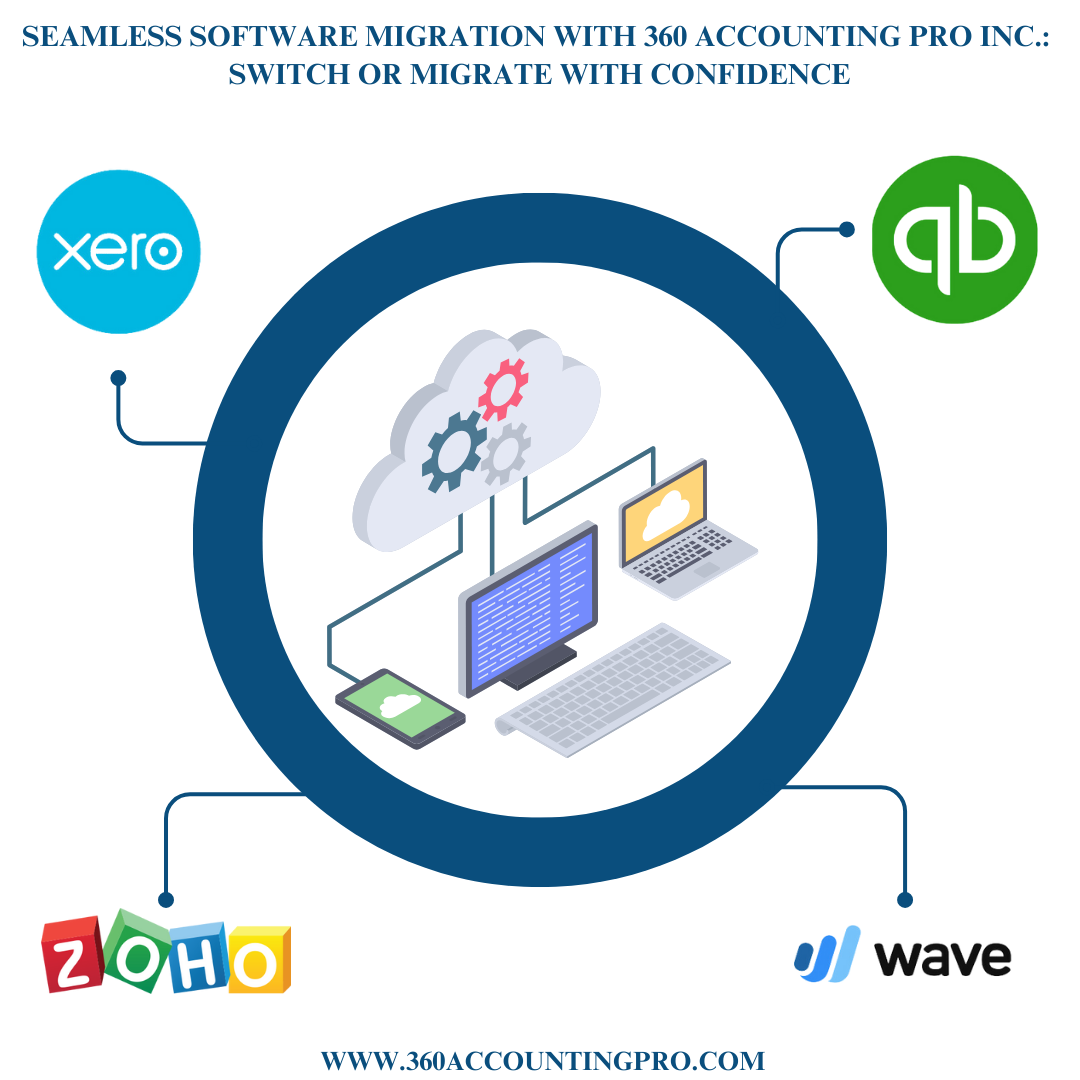

Not using accounting software since automating reconciliation with QuickBooks Xero or other software saves time

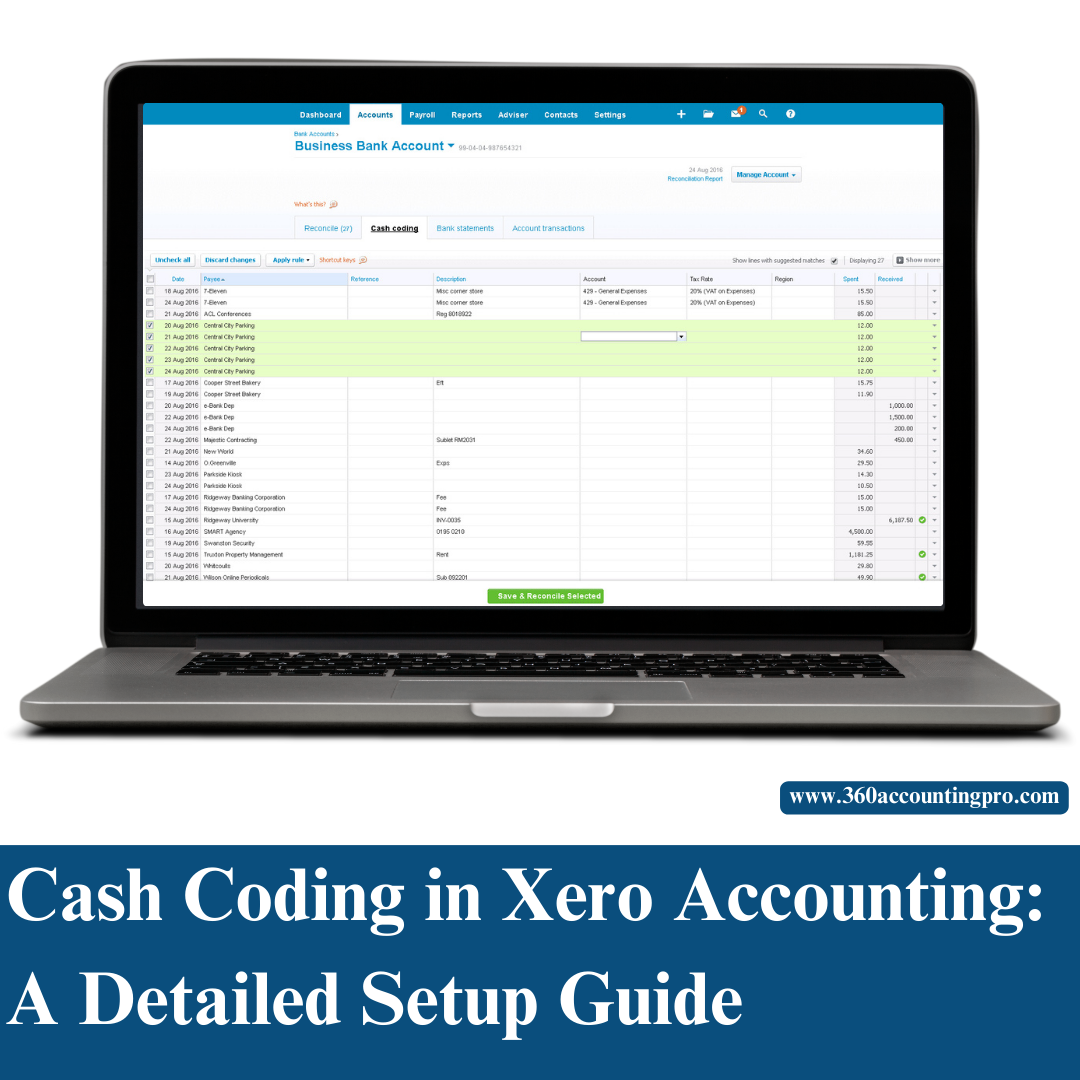

Many businesses use accounting software to streamline bank reconciliations. Here is how it works with popular platforms

QuickBooks allows users to connect bank accounts for automatic transaction imports use the reconcile feature to match bank records with accounting entries and generate reconciliation reports for review

Xero enables bank feeds for real-time transaction updates reconciles transactions using suggested matches and creates bank reconciliation summaries for reporting

Zoho Books automates transaction categorization for quicker reconciliation matches transactions with uploaded bank statements and identifies discrepancies with real-time alerts

Sage Accounting imports bank statements directly into the software reviews and confirms transactions in the reconciliation tool and adjusts bank balances based on missing or pending transactions

At 360 Accounting Pro Inc we offer expert bank reconciliation services to help businesses maintain accurate and up-to-date financial records

Automated reconciliation using accounting software for seamless bank reconciliations

Error detection and resolution by identifying and correcting mismatches

Customized financial reports to track profitability and cash flow

Regulatory compliance by ensuring accurate financial reporting and tax compliance

Learning how to do a step-by-step bank reconciliation is essential for accurate financial management. By following a structured reconciliation process and leveraging expert services from 360 Accounting Pro Inc businesses can improve cash flow accuracy reduce financial errors detect fraud early and stay compliant with tax regulations

Let our experts streamline your bank reconciliation process saving time and ensuring financial clarity.

Contact us today to learn how our reconciliation services can enhance business financial accuracy.

Tags : #BankReconciliation, #BankRecs, #AccountingTips, #FinancialManagement, #CashFlow, #FraudPrevention, #Bookkeeping, #AccountingProcess, #BusinessFinance, #FinancialRecords, #SmallBusinessAccounting, #BankStatementReconciliation, #ReconciliationProcess

.jpg)

.jpg)

.png)

.png)

.png)

.jpg)

.jpg)

.jpg)

).jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.png)

.jpg)

.jpg)

.jpg)

.jpg)

.png)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.png)

.jpg)

.jpg)

.jpg)

.jpg)

.png)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.png)

.jpg)

5.png)

1.png)

2.png)

3.png)

2.png)

4.png)

2.png)

1.png)

1.png)

3.png)

2.png)

1.png)

2.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

1.png)

1.png)

.png)

.jpg)

.png)

.png)

Get A Quote

Get A Quote

Leave A Comment